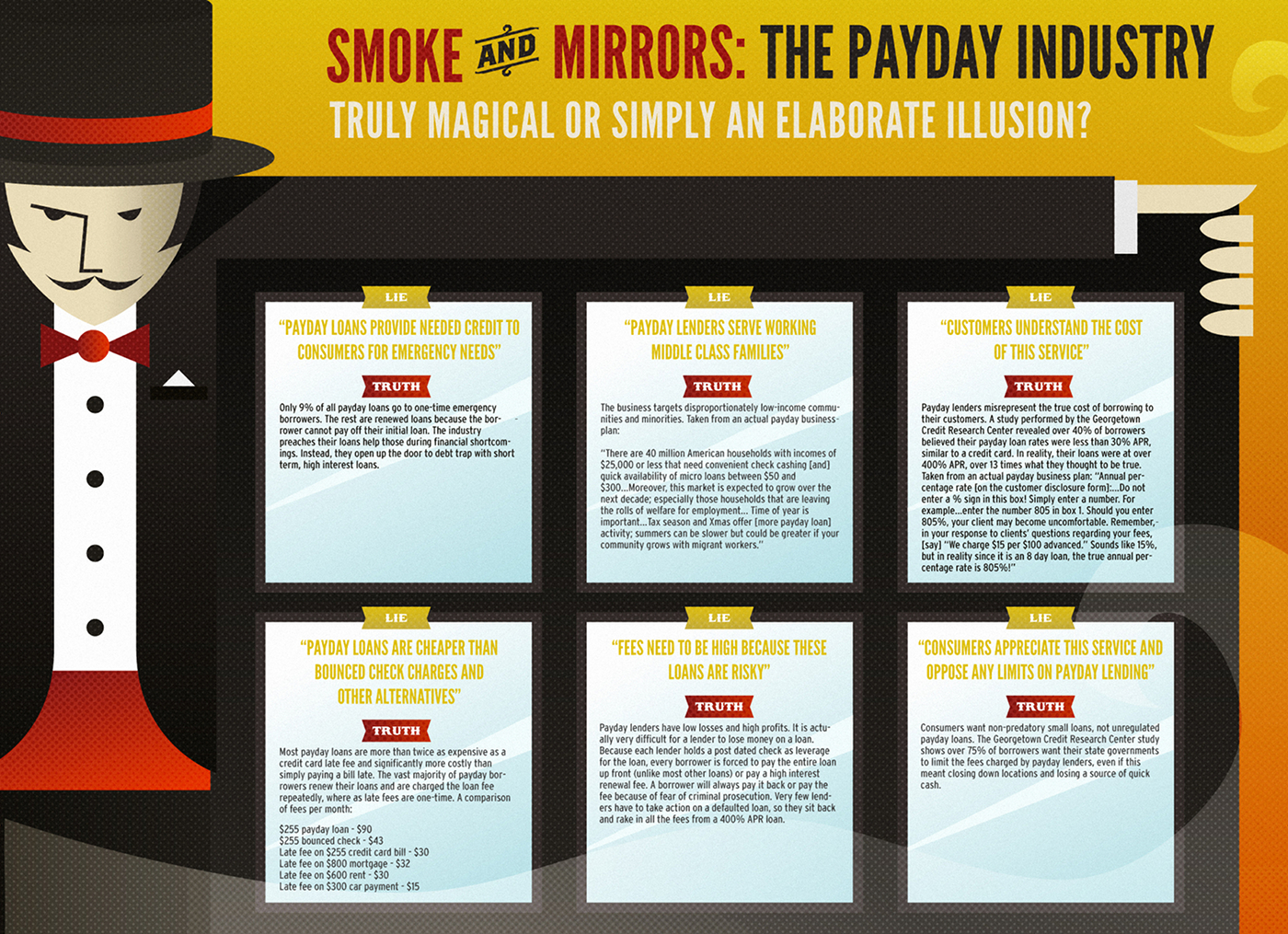

Payday loans were first legalized in the 1990′s. The idea is simple: Allow almost anyone to take out a small loan and charge them a flat fee with a short deadline. The average loan is $350 and average loan fee is over $50.

Borrowers write a personal check that is post dated and the payday location holds it until the original loan is paid off. The borrower must pay back the loan or they are forced to deal with a bounced check and other financial consequences.

Borrowers write a personal check that is post dated and the payday location holds it until the original loan is paid off. The borrower must pay back the loan or they are forced to deal with a bounced check and other financial consequences.

The majority of borrowers entrap themselves by never paying off the original loan and instead paying the loan fee to take out another loan to pay off the first. While this premise sounds bad enough, there are many other aspects of the payday industry that are just as shocking.

1. 76% of total loan volume comes from repeat loans

The payday industry operates in 35 states across nearly 23,000 locations. In the course of a year the industry generates $27.2 billion of loans. However $20.6 billion of the loan volume, 76%, derives from “churned” loans. A “churned” loan is defined as a loan made within the same two-week period in which a previous loan is paid off. Two weeks is the normal deadline for payday loans.

The vast majority of business stems from the borrowers inability to repay the original loan, causing them to immediately take another out and pay an additional fee. These are not one time loans, people become entangled in multiple loans and the fees begin to pile up.

2. The enormous amount of churned loans amounts to $3.5 billion in profit from fees

This is where the payday industry makes their money. Where your credit card only charges you interest if you fail to pay off the entire amount of a purchase, you pay upfront a flat fee to simply take out a loan. Since 76% of loans are repeat loans, the industry makes profit by getting the borrower to keep paying for loans because of their inability to pay off the initial loan. The average fee is $17.50 per $100 borrowed and for many this seems miniscule, but it adds up over the course of a year if not remedied.

3. There are two payday locations for every Starbucks

There are 11,000 Starbucks locations in America. There are 23,000 payday locations. So every time you complain or hear a complaint about the ridiculous number of Starbucks on every corner, take a second and understand there are twice as many payday locations in America.

4. In the 29 of 35 states where payday lending is legal there are more payday locations than McDonalds

Out of the 35 states that allow payday stores, there are 12,400 McDonalds compared to over 23,000 payday loan locations. Again, pretty shocking statistic considering we believe McDonalds to be one of the most ubiquitous businesses in our country.

https://www.csun.edu/~sg4002/research/mcdonalds_by_state.htm

5. The lowest APR cap is 156% in Texas and seven other states have no interest caps. The standard credit card APR is 16-18%

APR is annual percentage of rate. This is the interest rate for a whole year as applied to a loan. Basically, the APR calculates how much interest you pay if you borrowed the loan for a full year. For example, a payday loan fee of $17.50 per $100 for a two week loan equates to 455% (17.5% x 26 weeks).

Payday APR is astronomical compared to credit cards and other methods of borrowing. Payday locations trick potential borrowers by not revealing this statistic, instead focusing on the loan fee. Almost all borrowers do not realize the interest is in fact horrendous compared to other alternatives such as a regular cash advance or even loan from a friend for free.

6. $91.01 is the difference you pay by taking a payday loan versus a cash advance via credit card on a $300 loan paid in 30 days

Payday loan: $17.50 per $100 loaned, 15 day term with 1 rollover = $105 total fees

Cash advance via credit card – 20.23% APR with a 3% lending fee = $13.99 total fees

7. It’s frighteningly easy to obtain one of these loans

All a customer needs is a bank account, proof of income and identification. No location performs a full credit check or analysis to see if the loan is healthy in regards to the customer’s financial status. It’s harder to apply to many credit cards than it is to yank out a 455% APR loan.

8. Everything is due at once. You cannot make payments

This may not seem bad at first thought. Compare it to alternative loan methods and you see the disparity. Payday loans are short term loans that require you to pay back the entire amount or be forced to take out another loan.

Alternatively, many credit cards offer a grace period of repayment upwards of 30 days before any interest is charged. Even then, you can make small payments on purchases and combined with the relatively low APR on credit cards, this isn’t a big problem for most people. With payday loans, you are bound to pay the entire sum up front, so most people are forced to take another loan out immediately, thus paying the drastically high APR yet again. Either way, you are paying way more for a loan than you should be.

9. The industry constantly tries to undermine the law

Lots of lenders use sham transactions where they attempt to cloak the loans. An example is creating internet payday sites with rebate schemes that can avoid small loan laws in certain states. Texas lenders often operate as unregulated credit services organizations to blur their definition under state law. Locations in Illinois and New Mexico offer high cost installment loans instead of single payment loans to evade state law restrictions.

10. The industry targets minority neighborhoods

Statistics reveal in California payday lenders are eight times more concentrated in neighborhoods with the largest percentage of African Americans and Latinos. While the payday industry has been officially banned in North Carolina, many lenders still operate because of their affiliation with out of state banks. Of these that remain, they are three times more concentrated in the minority neighborhoods than Caucasian.

Information taken from https://www.paydayloaninfo.org and https://www.responsiblelending.org…

Read More